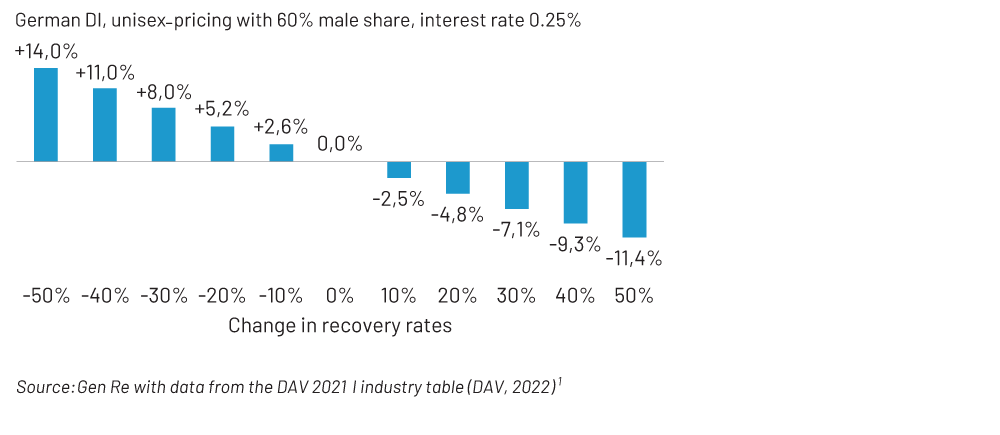

A permanent 30% increase in recovery, for example, could reduce premiums by 7% – this is significant, especially in times of shrinking margins. In terms of claims reserves, for those disabled at age 40 the claims reserve would be 9% lower.

Typical for an actuary, I have already bothered you with some figures on the subject. As a claims manager, you may be wondering: is there also concrete added value for your work, i.e., claims reviews, that actuaries can offer? I dare say the answer is ‘yes’; at least if we actuaries are ready to better understand some of the challenges of IP claims-handling.

For actuaries, this means that we have to communicate with non-actuaries – at first, it may sound like an effort, but it’s worth it! At Gen Re, claims managers and actuaries have teamed up to tackle the issue of claims reviews for German DI. Before we take a closer look at what came out of this, let me briefly outline what the typical German DI product looks like.

Long-term IP without deferred period

The German IP product (Berufsunfähigkeitsversicherung) has no deferred period, i.e., policyholders receive financial support from the first day of disability. But there is one crucial condition: medical evidence about the disability must be given, and it needs to be certified by a doctor and confirmed by the claims manager, that the disability is expected to last for at least six months. Hence, despite the absence of a deferred period, this is still a long-term Disability product. Most policies are sold in the individual business and usually cover the insured’s own occupation, i.e. provide financial protection if an individual can no longer perform the occupational duties they have been trained for.

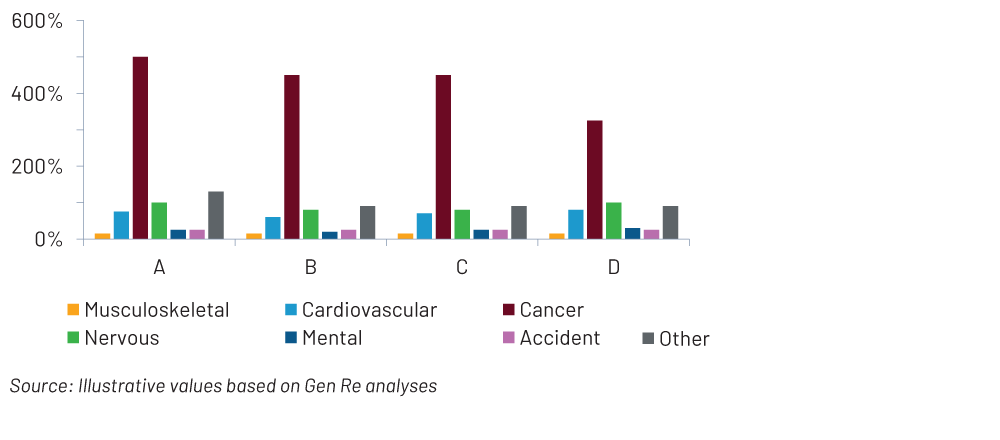

Traditionally, four occupational classes for IP policies were distinguished: from class A (very low risks) for e.g. office work with no exposure to hazards to class D (high risks) for e.g. heavy manual work. It has been shown that claims experience depends very much on the profession, making a more detailed differentiation appropriate. Today, insurers offer 12 occupational classes or even more.

Claims-handling for this product involves examining medical facts and considering the profession that the person held in healthy days. Against the backdrop of growing IP portfolios (which is positive in itself), the need for qualified claims managers is increasing. Finding a delicate balance between initial claims assessment and ongoing claims management is a challenge in many organisations.

How can actuaries support claims?

Trying to fully automate the claims management of complex insurance products does not sound like a good idea. It would probably cause more new problems than it would solve old ones. However, our actuarial data can help with prioritisation in the review process.

What do I mean by that? IP claims portfolios may comprise thousands of active Disability claims. To support claims departments in allocating their capacities, it would be great to assign some measure to active claims, indicating their suitability for review. The goal is to identify those cases with:

(a) A high probability of recovery

(b) A high (remaining) present value of benefits

Part (a) suggests that we should concentrate our efforts on cases with a good chance of success – in other words: not spend too much time on the claims that have a low probability of return to work. At the same time, cases should be economically significant. Suspending payments for individuals with minimal sums insured releases very few reserves. This is addressed by part (b).

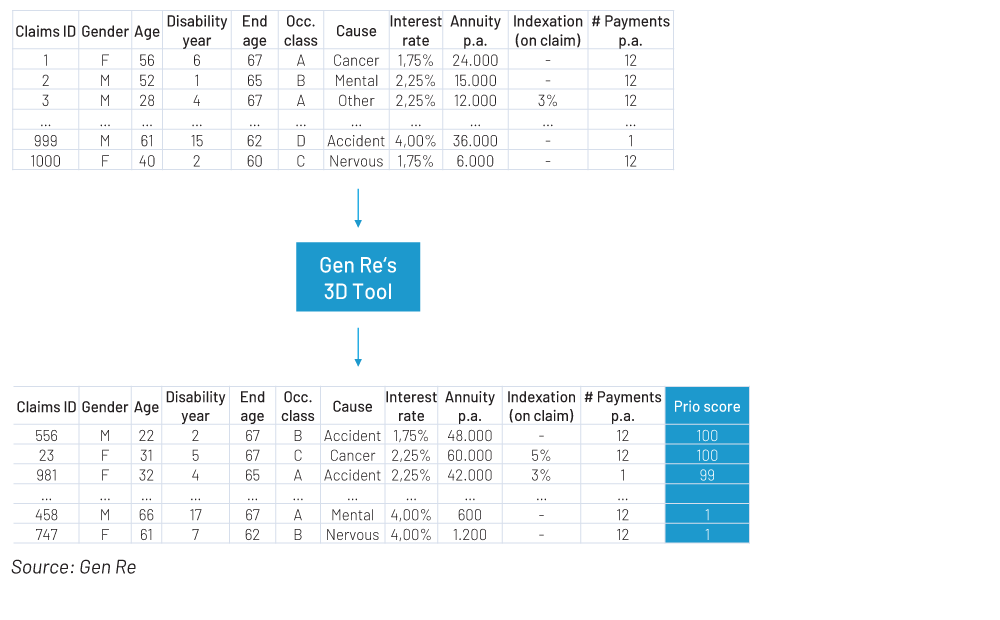

Experienced claims managers have a strong gut feeling for which claims (a) and (b) are high or low. On the other hand, they rarely have a comprehensive overview of the entire claims portfolio which would be essential for a systematic review process. This is where actuaries come into play. In collaboration with claims managers, we have designed the 3D Tool, the three Ds standing for “Data-Driven Disability” claims management.

Using statistical analyses, the 3D Tool determines on a best estimate basis (a) the probability of recovery within one year, and (b) the remaining present value of benefits, i.e., the expected total amount yet to be paid out. Both criteria – recovery chances and present value of benefits – are combined into a “prio score” ranging from 1 to 100. The higher the prio score, the more suitable an IP claim is for being reviewed: 1 indicates very low present value and (statistically) low chances of recovery; 100 indicates high present value and high chances of recovery.

The tool helps the claims department to allocate resources. If a claims department has the capacity to review, say, 30% of active cases, they could concentrate on the 30% with the highest prio score – and not assign resources on cases with a particularly low score. The actual reassessment of the claim, however, must still be carried out by the claims managers themselves.

The data behind the 3D Tool

As we aim for the most objective, systematised evaluation of a claims portfolio we need reliable statistics on a solid data basis. We use two sources for this: the new industry DI table (DAV 2021 I)2 and Gen Re analyses from our biometric data pools.

The new industry table for DI came into force in 2022, replacing the old DI table from 1997. The German Actuarial Association (DAV) is responsible for the derivation of this new table. It is based on the three big biometric data pools in Germany, run by Munich Re, Swiss Re, and Gen Re, which together cover 85% of the DI market – a splendid data basis!

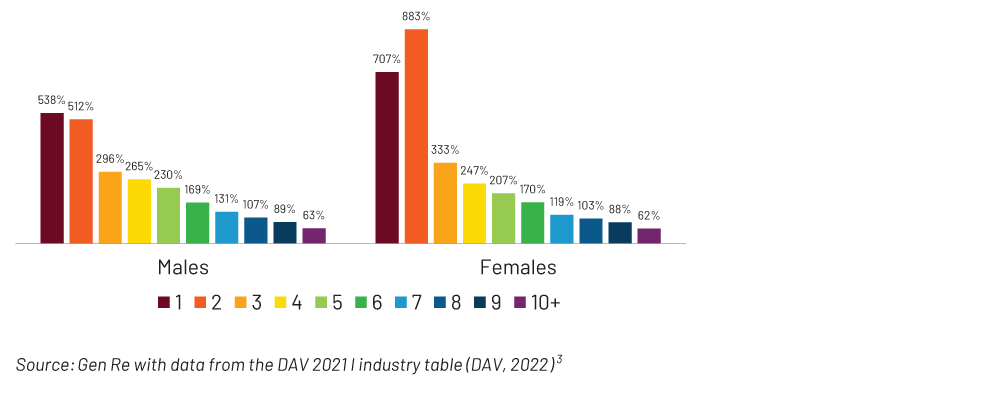

Besides incidence rates, which measure the probability of becoming disabled, termination rates are included – separately as recovery rates and mortality rates of the disabled. We need both: recovery rates go into our prio score directly and via the remaining present value of benefits; mortality rates of the disabled affect only the present value.

This gives us a good estimate of how the chances of recovery are influenced by three factors: age, gender, and years of disability. As shown in Figure 2, the probability of recovery for men in the first year of disability is 5.4 times as high as in disability years 6+; for women it is 7.1 times as high.

Figure 2 – Recovery by disability year in % of disability years 6+