- Property & Casualty

- Life & Health

- Knowledge Center

-

About Us

About Us OverviewCorporate Information

TOP

To discuss insurance fraud, let’s first understand what it is, and why we need to be concerned. As commonly defined: “Insurance fraud occurs when an insurance company, agent, adjuster, or consumer commits a deliberate deception in order to obtain an illegitimate gain. It can occur during the process of buying, using, selling, or underwriting insurance.”1 In order to prove that a fraud occurred, the following elements typically need to be met:

It’s important to remember that insurance fraud comes in many forms and can be committed at any stage of the insurance value chain, by any party involved along the way.

The true scope of insurance fraud is unknown since many incidents go undetected. Quantification can be difficult as accurate fraud statistics in certain parts of the world are hard to come by. However, we can infer the global scale of insurance fraud by looking at data from individual markets. For example:

U.S.

EU & UK

South Africa

India

Australia

Although insurance fraud is often thought of as a “victimless crime”, some fraudsters are known to finance other criminal activities with the fraud proceeds. For example, the money obtained through an insurance fraud scheme may be repurposed for offences such as drug or human trafficking, terrorism, etc. In fact, insurance fraud has enormous ramifications globally.

In order to identify insurance fraud, it’s important to understand the actors and their motives. Fraudsters are not confined to a particular demographic, nor a particular geographic region. Perpetrators may be organized crime groups or international syndicates, or simply “the person next door” – no matter their social background. Their motives can vary widely, with some cases being clearly premeditated and others merely taking advantage of a situation (e.g., padding/i.e., exaggerating the seriousness of an event).

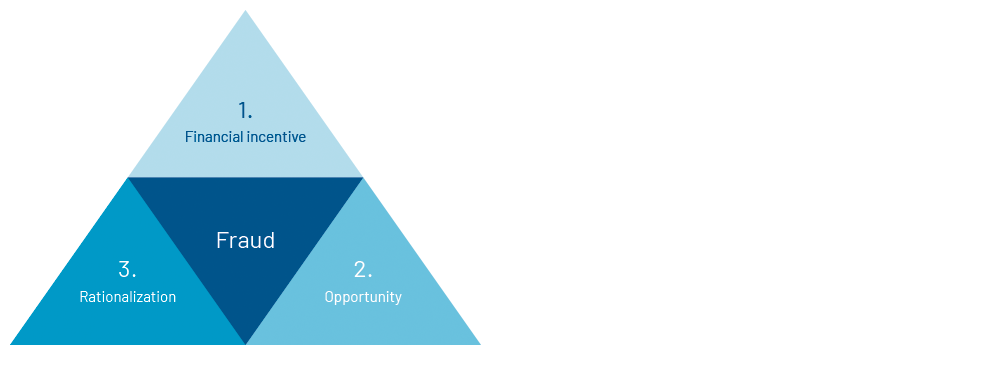

Although the individual motives and schemes may differ, most frauds contain the common elements of what is known as “The Fraud Triangle”.

Regardless of the perpetrator, the primary driver of insurance fraud is financial gain. Organized groups target insurers as part of their criminal enterprises as a means to make money and/or to fund other illicit activities. On an individual level, the financial drivers vary, but economic woes are a factor when considering motive. The cost-of-living crisis in various countries has been well publicized, and is linked to increased fraud rates in some areas. One UK insurer attributes a 31% jump in fraudulent property claims and a 7% rise in fake casualty claims in 2022 to cost of living challenges.10

Occasionally, people are lured into schemes with promises of quick, no‑strings financial rewards. A prominent anti-fraud agency in France, ALFA, recently reported on the proliferation of such cases being carried out via social media channels.11

The UK Insurance Fraud Bureau (IFB) published a study in 2022 that illustrates how economics and attitudes towards fraud intersect. Their data show that one in 10 people would consider insurance fraud if struggling financially. In the 18 to 24‑year-old age group, that number rises to one in five.12

If an individual with financial motive perceives an opportunity to achieve financial gain, they may decide to take advantage of an insurer’s processes and procedures. For example, they could choose to pad their claim, submit a false document, or provide other false information in order to profit. These opportunities may arise via streamlined underwriting or claims processes, or perhaps because the insurer lacks adequate due-diligence measures that serve as a control.

Organized groups will continually test insurers’ processes, looking for vulnerabilities that will allow them to exploit the enormous money-making opportunities associated with successful insurance scams.

Potential fraudsters will rationalize their choices by telling themselves that it’s not really stealing, and no‑one is getting hurt (i.e., it’s a victimless crime), or that the insurance company owes them a little extra in light of all the premiums they’ve paid over the years. Hypothetically, a desperate fraudster may need to pay their mortgage bill this month and falsifying an insurance claim is the only way they can keep their home.

Or perhaps an applicant realizes that they’d never be able to afford the premium for a much-needed Life policy if they admitted to prior nicotine use or past illnesses, so they conceal material information at the time of application.

The impact of fraud goes way beyond a simple “cost of doing business” and requires us to take steps to mitigate the impact. It’s everyone’s responsibility to be aware and take action so that we have multiple lines of defence in place.

Maintaining awareness, implementing controls, validating information, and stress-testing new processes will help limit our vulnerabilities. It’s also important that we know our customer. Ultimately, knowing the facts and knowing our customers helps us make better decisions.

Gen Re Germany’s Claims Visiting Service (CVS) is a great example of how we can achieve these goals. CVS is unique in that it provides us with an opportunity to meet with a claimant face to face in order to gather relevant information about that person’s situation. Through this program, our team can have direct conversations with claimants to better understand the circumstances surrounding complex matters.

Gathering information related to the “Who, What, Where, When, Why and How” improves our ability to objectively evaluate the merits of the claim. These detailed conversations also allow us to determine whether any discrepancies or suspicious loss indicators exist.

Whether we’re meeting claimants face to face (as with CVS) or whether we’re reviewing file materials remotely, it’s important that we’re able to identify the common industry-recognized suspicious loss indicators.

|

Industry-regognized suspicious loss indicators |

|

|---|---|

|

|

Proper identification and documentation of these indicators helps form the reasonable basis for us to take further action (e.g., request additional proofs, conduct a surveillance, interview witnesses, etc.). Documentation helps us explain to anyone (the claimant, their attorney, a regulator, etc.) why we are pursuing certain courses of action and helps mitigate our exposure to complaints or allegations of bad faith claim handling.

It is important to remember that the mere presence of a suspicious indicator should not be considered proof of fraud. The presence of suspicious indicators should prompt further inquiry as part of our fact-finding process. Concerns can be often resolved by asking the right questions.

The insurance industry faces enormous challenges when it comes to combating insurance fraud. Furthermore, data privacy and regulatory restrictions that impede information-sharing is a significant barrier to fraud mitigation efforts.13

A fundamental best practice for all insurance professionals is to maintain awareness of the trends, schemes, and suspicious indicators. The ability to identify suspicious indicators serves as a key control and is a vital first line of defence.

Insurance professionals should become familiar with, and utilize, the tools and information resources that are available to them in their market. The CVS Program is an example of an excellent resource (specific to the German market) that helps Gen Re with our Claims Risk Management processes – ensuring we pay what we owe.