A competing hypothesis is that wearables can become the cornerstone of future life insurance propositions. This premise requires two fundamental changes in behaviour: firstly, that insurers use personal data to enhance their customers’ wellbeing, and secondly, that customers will share their information on an ongoing basis because of the trust they have towards their insurer. These are two non-trivial changes that are necessary to change the face of life insurance going forward, but the possibilities are inviting. It also brings home the new ethos in data privacy: The individual owns his or her data and will share this data only with companies that provide value in return.

Life enablement

In moving into this new paradigm, insurers are responding to their customers’ changing habits, a phenomenon that is changing the nature of the contract between them. Insurers are no longer merely saying, “I will be there when something bad happens in your life”. Instead, the insurers’ are adding to their obligation in the contract and saying, “I will help you manage your life so that we can try and prevent bad things from happening, but when they do, I will see to it that you are best placed to deal with what needs to be done”. Another way of describing this change in paradigm is moving both the insurer and the customer from a “What if” to a “So, how?” mind set. Thus, the customer, with the insurer’s input, will be asking, “So, how will I be able to deal with this debilitating disease?”, or “So, how can I improve my cardiovascular health?” This alternative paradigm and that of “what needs to be done” are emerging themes in the Incredible Curious Global Adventure video project. Life insurers then become life enablers, to the benefit of their customers, their customers’ families, employers, society and themselves.

Underwriting

In the insurance industry, attention is focused on underwriting because technology firms are challenging the norm. We are asking whether data from wearables could supplement or even replace the traditional underwriting journey. Or equally, why does underwriting only happen once at the beginning of the contract and never again? This was never easy or cheap to do in the past, but the rapid growth in the number of wearables and sensors, the range of metrics they record, and the ease of sharing the data has changed the dynamic.

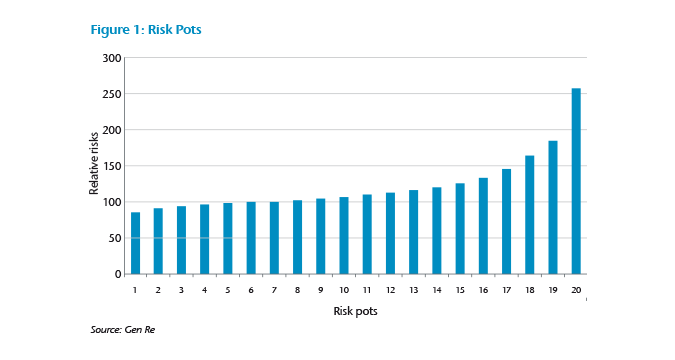

HealthyHealth, Torafugu Tech and PAI Health have used academic research to develop risk scores that measure the relative risk of the person to certain metabolic and cardiovascular diseases. All three companies understand the change to the new paradigm: Sharing such information must be of value to the customer as well as the insurer. They have all built user interfaces to communicate scores to users with information on how they can improve health outcomes for themselves. HealthyHealth uses smart devices to collect and analyse lifestyle data on exercise, nutrition and vital signs, and its algorithms translate this data into personalised health and lifestyle improvement plans that use cognitive methods to engage customers.

PAI Health uses links with high grade wearables to measure the body’s response to the intensity and duration of physical activity by translating heart rate data into a single, accurate, meaningful metric that provides guidance and motivation to maintain optimal health. The approach uses the person’s own baseline score as a basis for all future measurements. Torafugu has identified links between activity levels and metabolic diseases, such as diabetes, and uses similar cognitive techniques to assist its customers to improve behaviour and outcomes.

It will take time to replace the traditional underwriting approach purely by using wearables, but as the data emerges and is amalgamated with data from the existing process, this will help us to create richer and more relevant underwriting processes in the future.

Claims

Apart from the life-enabling aspects set out above, technology can help policyholders when they need to submit a claim. Many insurance companies have developed apps that customers can download and use to notify claims, to submit supporting data, to track progress and receive decisions on claims. A few insurers are investigating the possibilities of providing support and guidance remotely, thereby prompting some of the new technology provider companies, which understand the customer-centric view required, to direct their clinical apps into the insurance space in collaboration with Gen Re.

Companies generating health solutions to support claims

Monsenso is a mobile mental health solution for engagement, monitoring and active support based on self-assessment, data from phone sensors, and physical and social activity data. Its services help clinicians support the mental health of patients remotely. In clinical use, it provides insights to caregivers and physicians through aggregated data and provides patients with support, feedback and even cognitive behavioural therapy (CBT). The underlying philosophy is that mobile technology allows for real time support for patients. Once again, having established a baseline for a patient’s behaviour and activity, deviations from that norm can be monitored and identified, prompting appropriate and timely intervention and support. This process is a lot more powerful than the regular monthly or two monthly visits to the clinician.

Thrive is another company with a similar approach in this area. Thrive is a confidential wellbeing app that helps build resilience, prevent and manage stress, anxiety and other common mental health conditions – and proven to accelerate recovery.

Both of these approaches have also been shown to facilitate a better return-to-work experience.

Digital approaches can also provide support to customers in rehabilitating musculoskeletal injuries. Some companies, including AIMO and TrackActive, are also using the power of visual digital technology to enhance the experience and to facilitate improvement.

AIMO is a preventative health solution that links the power of a smartphone to analyse movement data in an automated movement analysis platform. AIMO uses visual digital technology, leveraged through a downloadable app, to identify limitations in the movement of the person and then to create exercises that address that limitation. A 3D depth camera uses movement data to identify and score complete movement patterns, data that is used to compute individualized analysis and recommendations, such as training, treatment and equipment. It aims to help insurers engage with customers and reduce health claims costs, and could be applied to musculoskeletal claims or to underwriting.

TrackActive is an AI engagement platform that provides early, cost effective and scalable interventions for rehabilitation and prevention of musculoskeletal conditions and chronic disease. By directing users to the most appropriate and convenient method of managing their conditions, it aims to improve engagement and speed recovery by delivering and monitoring exercise and rehabilitation. TrackActive has developed a complementary service that uses downloadable videos to show the customer exactly how to go about the relevant exercise to ensure no further damage and improve chances of a fuller recovery.

In conclusion

Lasting change will come from truly understanding our customers’ needs and designing processes to help them to deal with the issues they are facing. Emerging technologies, including voice recognition technologies, will enable insurance companies to “get the job done” easily and conveniently, whether the technologies provide underwriting information or notification of claims. But this innovation in life and health insurance can only happen through a collaboration between reinsurers, insurers and new tech businesses, where each party brings its insights and skills together for the ultimate benefit of the customer.