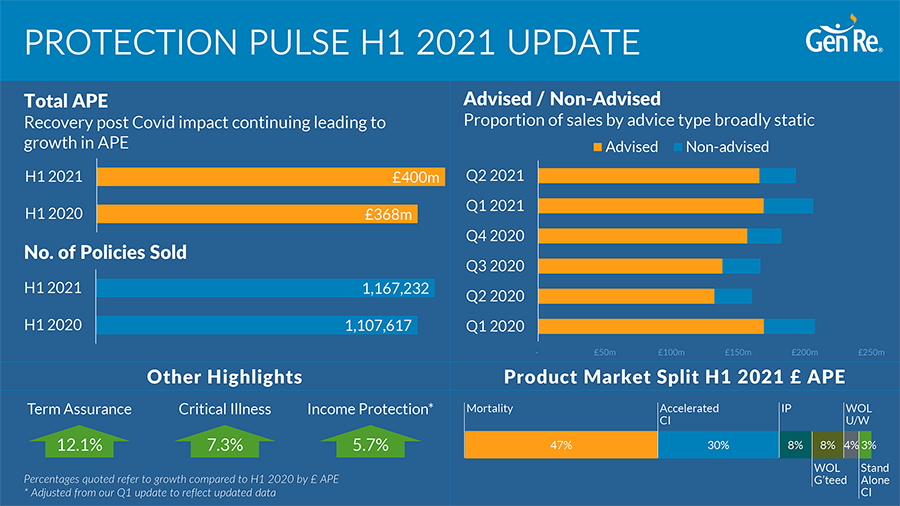

Since the start of the Covid‑19 pandemic more than 18 months ago, there has been considerable volatility in the level of protection sales, with the various product lines impacted to differing degrees. Sales during the first half of the year have proven no exception.

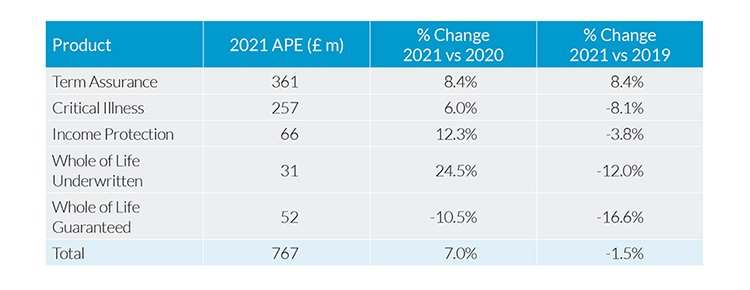

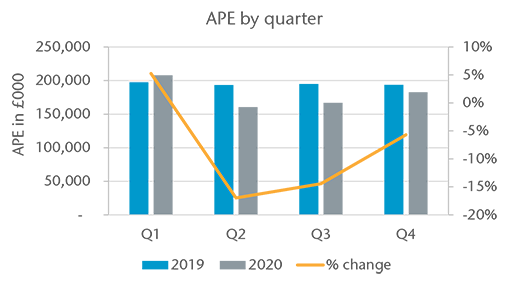

However, despite the UK having had some degree of restrictions over the whole of the first half of the year, H1 had the highest level of protection sales in recent times, with sales even higher than in 2019. This is especially encouraging given the harsh environment the industry has faced. Overall sales are up 8.6% from the first half of 2020 and 2.4% up from the first half of 2019.

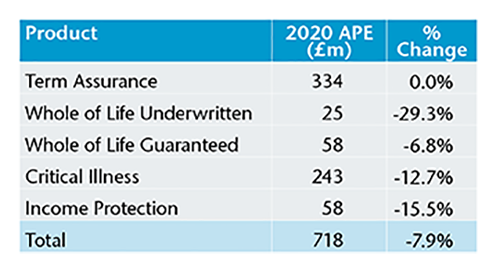

At a product level, the major driver of the increase is Term Assurance sales, which are up 12.1% compared to the same point in 2020, and 14.3% up against the 2019 position. This continues the growth seen in recent years for this product. This should not come as too much of a surprise. According to the government national statistics, we saw more homes sold in Q1 of this year in the UK than any other period reported since 2005.1 The demand for housing was at an all-time high as buyers looked to purchase properties that better suits their revised needs, and before the temporary stamp duty relief ended on 1st October 2021.

Also performing well is the standalone critical illness, which has continued to grow despite the pandemic: H1 sales are 8.7% higher than at the same point in 2020, and sales have now increased for five successive half year periods. Accelerated CI, on the other hand, is performing less well: although sales increased in 2021 by 7.2%, premium levels are below that of 2017, with the 15% reduction in 2020 sales having a significant impact.

Income Protection was another product that had a fall due to the pandemic, with a reduction in sales of 14% in 2020; the first half of 2021 had sales increasing by 5.7%, although premium levels are still c. 5% below that of 2019. As the economy continues to recover and with the furlough scheme finishing in September, we hope to see a return to the growth levels seen pre‑pandemic.

Guaranteed Acceptance Whole of Life sales are comparable to that of the corresponding first half of 2019 and 2020. However, underlying this is a very strong Q1 but a weak Q2, with the drop-off of Q2 sales far greater this year than historically, with a 38% reduction compared to a more typical 15% between these two quarters. We will continue to monitor this to see if this is a one-off or a systemic change. Sales of the underwritten Whole of Life continues to decline: whilst there was a 9.2% increase in premium income during the first half of the year compared to 2020, sales are c. 40% down from the 2015 level. It remains to be seen whether the removal of some of the underwriting restrictions that were introduced during the Covid pandemic will help boost sales.

With the restrictions in the UK having eased on the 19th July and the early positive trends we are seeing, we remain optimistic that the industry will bounce back in the second half of the year as the recovery gathers pace, and with the Covid‑19 pandemic hopefully becoming under control.

Endnote

- https://www.gov.uk/government/statistics/monthly-property-transactions-completed-in-the-uk-with-value-40000-or-above