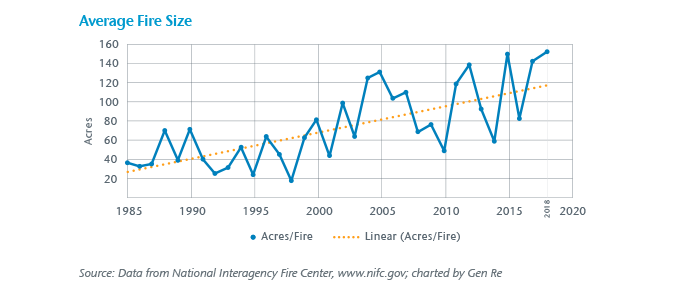

Over the last five years, we’ve seen a tremendous increase in losses from wildfire activity. That activity has been heavily concentrated in California, which accounts for seven out of the 10 largest wildfires in terms of structures impacted. That activity has also elevated wildfire, formerly considered a minor or secondary peril for insurers and reinsurers, to a primary catastrophe peril at the level of hurricane, earthquake, flood, and tornado.

Growing and Spreading Risk

A major factor in the increase in structural losses due to wildfire can be attributed to the rapid increase in structures built in the Wildland Urban Interface (WUI) – defined as “a set of conditions and interactions within the built and natural environments that increase communities’ vulnerability to wildfire.”1 Unfortunately, the statistics on WUI growth are not considered a completely reliable and up-to-date record. The last formal study was released by the USDA in 2015 but it relied on 2010s “as of” data.

The normal fluctuations of climatic conditions, potentially exacerbated by climate change, have had many unexpected and unique regional impacts that contribute to increased wildfire exposure. Also, the persistent infestation of bark beetles, that appear to be leaving dead trees behind in an increasing rate, provides more fuel for wildfires. These overlapping stressors are often mentioned as causes contributing to the perceived increase in wildfire frequency and severity.

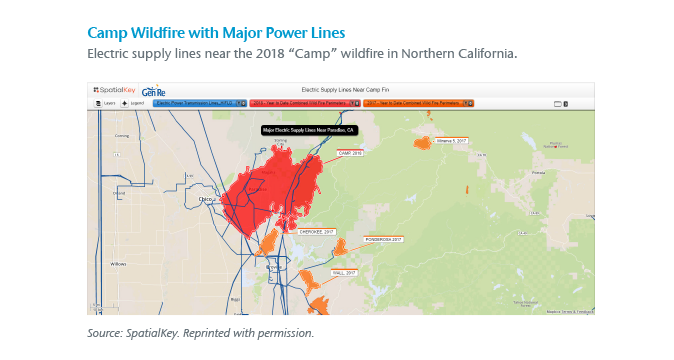

Another factor receiving a lot of attention is the impact of power utility operations and related infrastructure maintenance practices. The human element (e.g., poor forest management around power lines) has been noted as causing and amplifying initial ignition, intensity, and duration of recent wildfire events. The problem is not new. Over the last decade, legal judgments and successful insurance subrogation have obtained recoveries from utilities for wildfire damages.

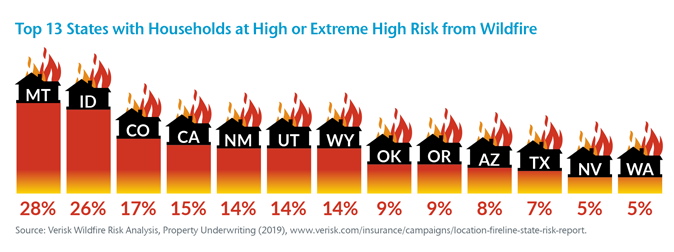

With the recent wildfire losses, California has been the focus of much of the industry’s concern – and rightfully so, given the high number of high-risk households (15% of the total number of households) in that state. However, other Western states have a much higher percentage of households exposed to wildfire at a high or extreme risk level (28% for Montana). To illustrate, see our compilation of the Top 13 states at high risk, as reported by ISO Verisk.2

Tools and Challenges

Until now, the risk evaluation and aggregation tools used for wildfire peril were, for a variety of reasons, relatively unsophisticated compared to more mature underwriting tools and models developed for hurricane and earthquake perils. Third-party modeling firms don’t spend resources developing Cat models unless there is a clear demand and financial support from the insurance industry. However, in response to increased wildfire activity in recent years, the insurance industry and third-party model vendors are now channeling more resources into improving the knowledge and understanding of this peril. The goal is the development of tools for better risk evaluation, projected loss modeling and more accurate aggregation of exposed values.

One current limitation in existing tools is the incomplete historical record of physical wildfires, acres burned, wildfire-related structural losses, and human loss of life. The reason is that there is no comprehensive consolidated dataset of historical fire activity akin to the extensive wind and storm records that can be accessed through NOAA. The most complete and consistent records are based on wildfire activity within federal lands. In contrast, many individual municipalities have their own independent protocols for fire reporting and records. They do not generally overlap and may result in significant gaps between the local and federal fire experience data.

Another weakness identified in our research is the use of traditional geopolitical map aggregation zones (county, town, ZIP code) for exposure management, as compared to wildfire peril behavior which doesn’t follow traditional map boundaries.

Wildfires tend to be rural in nature and have a high percentage of total losses to structures due to the lack of fire protection resources. Whereas other natural catastrophe perils, such as hurricane and earthquake, are predominantly partial loss scenarios spread over more loss locations and a much larger geographic footprint. The high individual loss severity characteristic of conflagration losses contributes to the relatively large dollar losses from wildfire events.