When restaurant or bar operations are considered for insurance, we automatically think about fires, liquor liability and workers' compensation. That is a tried and true start. But underwriters beware! Breweries, wineries and distilleries present additional and sometimes unique exposures of their own.

What additional risks should be considered for craft alcohol business?

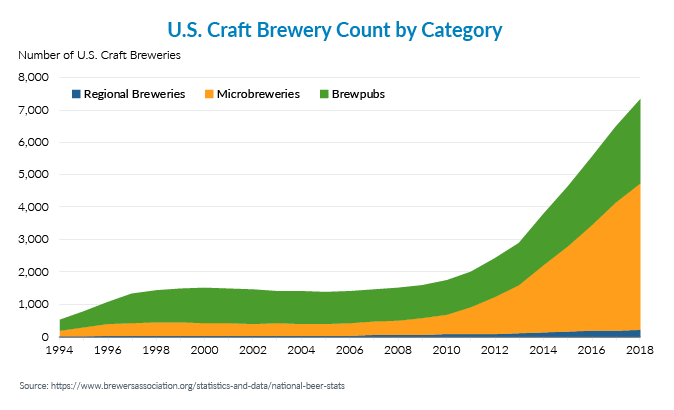

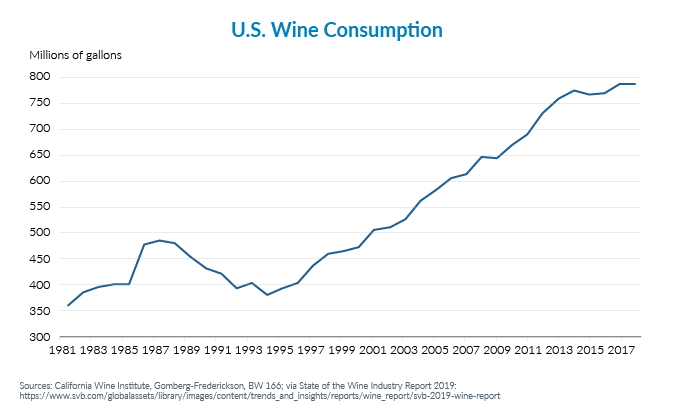

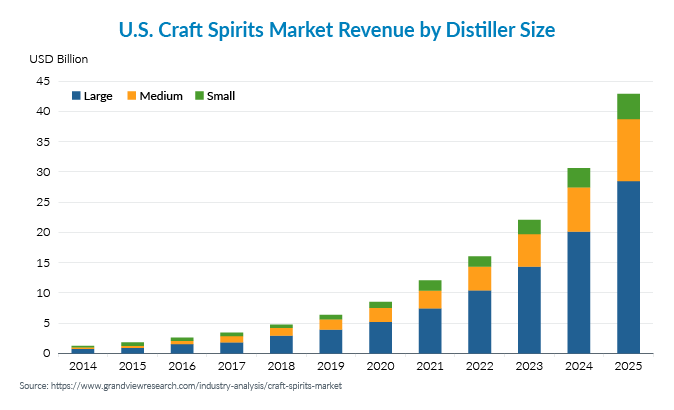

To understand the exposures as well as marketing opportunities, we note that these craft alcohol businesses are still enjoying strong growth across the country. No doubt you have observed several opening in your area over the past five or so years. These graphics tell the story.

Makers may be concerned that the availability of legal marijuana will depress demand for their output - but there is no sign of that in the latest numbers.

7 Liability Exposures to Contemplate

- Explosions and Tourism - Major distillery explosions in the U.S. have caused substantial property damage and personal injuries, usually involving employees. With the growth of on-site tours and travel groups devoted to craft alcohol, more and more visitors are exposed to injuries. One recent brewery tank explosion sent suds throughout the premises and several visitors sued for injuries. Does the physical layout separate guests from machinery? How close are neighboring properties?

- Children on Premises - Visit a craft alcohol website and you may be asked if you are over 21. Then why do many establishments permit children on the premises? Some limit hours or enforce a flat ban. But those allowing children report scenarios where parents engaged in tastings and activities lose sight of their kids, leading to dangerous situations. In one case, the manager found a seven-year-old climbing outdoor scaffolding erected for an upcoming music festival. What measures are in place that focus on the security and safety of kids?

- Entertainment/Agritainment - Rock concerts, weddings, benefit galas, Oktoberfest, hayrides…In the competitive environment of craft alcohol, makers are introducing more risks in on-site and off-site activities to attract customers. While some activities are rather benign (book clubs, paint and sip, lawn games), others can generate rowdy crowds that can get out of control. Size limitations and hours of operation are critical factors impacting this exposure. Another is the age of employees overseeing these activities. Is a summer college student evaluating the sobriety of guests driving the hayride tractors?

- Food Contamination - While alcohol is the core business and the product is presumably monitored closely for contaminants, the same may not be true for the monitoring of food served on the premises. Events may be catered or food trucks may come by at meal times, or in some cases the brewery or winery cooks the food on-site. Some offer cooking and related classes. What about warm days when trays of salads and sandwiches sit out in the sun while guests play lawn games or listen to the local band? Relative to alcohol exposure, these products have just as much or more risk - in food contamination exposure.

- Retail - Selling their product is part of the pride and decor vibe of these facilities. Bottles often sit in open air shelving that is crowded with patrons. Can underage visitors on the premises for food or a concert access the alcohol? How closely is inventory monitored?

- Slips and Falls - While beer spills on the dance floor can cause falls, the overall slip and fall risk is probably lower than for the typical restaurant. The buildings tend to be newer and spread across one level, although that can vary considerably by geographic area. When they feature ramps and elevated walkways for better viewing, they certainly increase their risk. However, a guest probably won’t need to walk down a poorly marked or low-lit stairwell to find the rest room in the basement.

- Related Operations - As craft businesses have grown, many owners have capitalized on that demand to establish lodging, catering, transportation, travel and other entities. Customers may not be aware of the business inter-relationships, but insurers should be. How are these entities covered and what is the contractual relationship within the corporate family? Coverages should be structured to avoid multiplying limits exposed.

Insurers might be tempted to underwrite and rate some of these craft alcohol establishments as manufacturing risks. As you can see, the premises exposures may be an even greater source of claim activity. The typical insured has significant premises, products and dram shop liability laced with frequency and severity risk.

Check out the website of a brewery, winery or distillery near you. There are probably more facilities than you expected, and almost certainly more activities on the schedule.

Bottoms up!